Table of Contents

- 1. Chile’s fintech sector matures with strong B2B growth

- 2. Market Maturity and Growth of Fintech in Chile

- 3. Regulatory Environment Supporting Fintech Innovation

- 4. Leading Payment Gateways for B2B Transactions

- 4.1 NOWPayments: The Top-Rated Gateway

- 4.2 PayPal: A Global Leader in B2B Payments

- 4.3 Mercado Pago: Regional Dominance

- 5. Emerging Trends in B2B Payment Solutions

- 6. Cross-Border Payment Platforms for Chilean Businesses

- 7. Local Startups Innovating in B2B Payments

- 8. Investment Landscape for B2B Fintech in Chile

- 9. Future Trends in B2B Payments and Collections

- 10. Final Thoughts on B2B Solutions in Chile

Chile’s fintech sector matures with strong B2B growth

- Chile’s fintech market is more mature in 2026, with steadier growth and higher transaction volumes.

- B2B is now a core focus: in 2024, nearly 64% of fintechs targeted business customers.

- Open Finance, multi-acquiring, and stronger cybersecurity standards are reshaping payment infrastructure.

- Gateways like NOWPayments, PayPal, and Mercado Pago lead, while platforms like HighRadius push cross-border automation.

Chile Fintech Shifts to B2B

– B2B focus shift: In 2024, nearly 64% of Chilean fintechs targeted business customers vs 27% in 2021. (Galileo-FT, 2024: https://www.galileo-ft.com/blog/chile-evolving-fintech-market-insights/)

– Payments scale-up: 42.9% of payment fintechs surpassed US$100M in transaction volume in 2024 (up from 25% in 2022), with a projection of 60.7% by 2025. (Galileo-FT, 2024)

– Infrastructure direction: 2026 coverage highlights Open Finance, multi-acquiring, and cybersecurity as the trust layer behind modern payment methods. (Evertec, 2026: https://evertectrends.com/en/payment-methods-in-2026-the-year-trust-becomes-infrastructure/)

Market Maturity and Growth of Fintech in Chile

Chile’s fintech sector enters 2026 with a clearer signal of maturity: less volatility, higher penetration, and rising transaction volumes—especially in payments and remittances. What stands out is how decisively the ecosystem has pivoted toward business use cases. In 2024, nearly 64% of Chilean fintechs targeted business customers, a sharp change from 2021, when only 27% served large corporations and financial institutions. (Galileo-FT, 2024: https://www.galileo-ft.com/blog/chile-evolving-fintech-market-insights/)

That shift matters because B2B payments and collections are operationally demanding: reconciliation, invoicing, compliance, and multi-rail acceptance are not “nice-to-haves,” they’re table stakes. The market’s growth is also visible in scale. In the payments and remittances segment, 42.9% of payment fintechs surpassed US$100 million in transaction volume in 2024, up from 25% in 2022, with projections pointing to 60.7% by 2025. (Galileo-FT, 2024)

For mid-sized companies and enterprises, this maturity translates into more choice—and more specialization. Alongside global brands, Chile now supports a layered stack: payment gateways, bank-transfer specialists, ERP/POS suites with electronic invoicing, and cross-border automation platforms. The result is a market where “B2B payments” increasingly means an integrated workflow: collect, match, reconcile, post to the ledger, and prove compliance.

| What changed | 2021 | 2024–2026 signal | Why it matters for B2B finance teams |

|---|---|---|---|

| Fintechs targeting business customers | 27% | ~64% | More vendors are building for invoicing, reconciliation, and enterprise controls (not just consumer UX). |

| Payment fintechs above US$100M transaction volume | 25% (2022) | 42.9% (2024); 60.7% projected (2025) | More providers operating at scale—typically a prerequisite for reliability, integrations, and support maturity. |

Regulatory Environment Supporting Fintech Innovation

Chile’s regulatory posture is widely viewed as among the most fintech-friendly in Latin America, and by 2026 it is reinforcing a key theme: trust is becoming infrastructure. The rollout of Open Finance, the adoption of multi-acquiring models, and the push for enhanced cybersecurity standards are shaping how B2B payments are built, sold, and operated. (Evertec, 2026: https://evertectrends.com/en/payment-methods-in-2026-the-year-trust-becomes-infrastructure/)

Open Finance and interoperability are particularly relevant for B2B. When payment providers, banks, and fintechs can connect more cleanly, businesses can reduce dependency on a single rail or acquirer and design more resilient collections strategies. Multi-acquiring, in turn, supports redundancy and optimization—important for companies that cannot afford downtime, failed authorizations, or rigid pricing.

Regulatory maturity also raises expectations. As transaction volumes grow and scrutiny increases, security and compliance become non-negotiable. Leading platforms are embedding controls directly into payment workflows—covering areas such as AML, KYC, and PCI DSS—so compliance is not bolted on after the fact, but enforced as part of day-to-day operations. (HighRadius, 2026: https://www.highradius.com/resources/Blog/best-cross-border-payment-platforms/)

Modern Payments and Risk Drivers

– Open Finance (plain-language impact): Makes it easier to connect accounts, payment data, and financial workflows—so collections can be tracked and reconciled with fewer manual exports/imports.

– Multi-acquiring (plain-language impact): Lets businesses route transactions across more than one acquirer/processor—useful for redundancy, negotiating leverage, and optimizing approval rates.

– Cybersecurity standards (plain-language impact): Push providers toward stronger controls and monitoring—reducing operational surprises (chargebacks, fraud spikes, account takeovers) that show up as reconciliation and dispute workload.

For Chilean businesses, the practical implication is straightforward: vendor selection is no longer only about acceptance rates and fees. It’s also about whether a provider’s architecture and controls can support audits, cross-border requirements, and operational scale without forcing finance teams into workarounds.

Leading Payment Gateways for B2B Transactions

This overview focuses on B2B collections and payments solutions referenced in 2026 market coverage, spanning payment gateways, ERP/POS suites with electronic invoicing, cross-border automation platforms, and local startups operating in Chile.

Chile’s gateway landscape in 2026 reflects two realities at once: the continued importance of global networks and the strength of regional platforms tuned to local preferences. For B2B merchants, gateways are often the front door to collections—supporting cards, bank transfers, wallets, and increasingly, alternative rails.

Below is a snapshot comparison of leading options referenced in 2026 market coverage. (NOWPayments, 2026: https://nowpayments.io/blog/payment-gateway-chile)

| Provider | Supported Assets | Fees | Transaction Speed | Integration | Instant Payout |

|---|---|---|---|---|---|

| NOWPayments | 350+ crypto, Visa, Mastercard, PayPal | 0.5–1% | Instant | Easy, e-commerce | Yes |

| PayPal | Cards, PayPal, bank transfers | ~3.49% + fixed, conversion | Instant–minutes | Global, e-commerce | Yes |

| Mercado Pago | Cards, bank transfer, wallet, QR, cash | ~2–5% | Instant | Regional, e-commerce | Yes |

| Khipu | Bank transfers | Variable | Instant | Local | Yes |

| PayU | Cards, bank wires, wallets | Variable | Instant | Global, scalable | Yes |

Italic caption: Comparative overview of leading payment gateways used in Chile (2026).

The “best” gateway depends on what a business is optimizing for: cost, acceptance, cross-border reach, local payment methods, or the ability to add new rails quickly. In practice, many B2B companies end up with a blended approach—pairing a globally recognized option for international clients with a locally optimized provider for domestic collections.

NOWPayments: The Top-Rated Gateway

NOWPayments is positioned in 2026 as a top-rated gateway option in Chile, largely because it spans both conventional and crypto rails in a single integration. For B2B sellers, that flexibility can matter when serving a diverse client base—some paying with cards and others seeking digital-asset settlement.

Its coverage includes 350+ cryptocurrencies alongside Visa, Mastercard, and PayPal support. Pricing is listed at 0.5% when no exchange is required and 1% when conversion is involved. The platform also highlights a promotional detail: 0% network fees on USDT TRC20 deposits for two months, which may be relevant for businesses experimenting with stablecoin-based flows. (NOWPayments, 2026: https://nowpayments.io/blog/payment-gateway-chile)

Operationally, NOWPayments emphasizes instant confirmation and settlement, plus instant payouts, and “easy integration” with e-commerce platforms. In B2B contexts, speed is not only about customer experience; it affects cash forecasting and reduces the window where payments are “in limbo” and harder to reconcile.

The trade-off is strategic rather than purely technical: adopting crypto-capable rails increases the need for clear internal policies on acceptance, conversion, and accounting treatment—areas where finance teams typically want predictable processes.

PayPal: A Global Leader in B2B Payments

PayPal remains a default choice for many cross-border B2B scenarios because it combines global brand recognition with broad payment method support: credit/debit cards, PayPal balance, and bank transfers. In 2026, that trust factor still matters—especially when a Chilean business is selling to international clients who prefer familiar checkout and buyer protections.

The cost profile is typically higher than some alternatives, with fees cited around ~3.49% plus variable fixed fees, and potential currency conversion charges. For B2B, those fees can be acceptable when PayPal is used selectively: for example, for international invoices where conversion, settlement speed, and customer confidence outweigh pure processing cost. (NOWPayments, 2026: https://nowpayments.io/blog/payment-gateway-chile)

Transaction speed is generally instant to a few minutes, which supports fast confirmation and reduces friction in order fulfillment or service activation. PayPal is also commonly integrated into e-commerce and online billing flows, making it a practical layer for companies that need to start collecting quickly without heavy implementation.

In short, PayPal’s value in Chile’s 2026 B2B stack is less about being the cheapest rail and more about being a globally legible one.

Mercado Pago: Regional Dominance

Mercado Pago’s strength in Chile is its regional footprint and its alignment with local payment behaviors. For B2B companies that sell across Latin America—or that need to accommodate a wide range of domestic payment preferences—its ecosystem approach is a major advantage.

Supported methods include Visa, Mastercard, debit cards, bank transfers, a digital wallet, QR payments, and cash options. Fees are cited in the ~2–5% per transaction range in Chile, reflecting the reality that broad acceptance and convenience often come with a higher blended cost than bank-transfer-only solutions. (NOWPayments, 2026: https://nowpayments.io/blog/payment-gateway-chile)

For B2B, Mercado Pago can be particularly useful when collections are not purely “invoice and wire transfer,” but involve mixed channels: online checkout, QR-based payments, or wallet-based flows. Its integration strength—especially in e-commerce and retail-adjacent environments—helps businesses unify acceptance across customer segments.

The benefit is reach: Mercado Pago can reduce the operational burden of stitching together multiple local methods. The risk is concentration: relying too heavily on a single ecosystem can limit negotiating leverage, which is why multi-acquiring and interoperability trends are closely watched.

Emerging Trends in B2B Payment Solutions

Three themes define B2B payments in Chile in 2026: interoperability, embedded compliance, and automation.

First, Open Finance and interoperability are changing expectations around connectivity. Businesses increasingly want payment providers that can plug into broader financial workflows—supporting transparency, data portability, and resilience. The move toward multi-acquiring reinforces this: rather than being locked into one acquirer or one rail, companies can design redundancy and optimize routing based on cost or performance.

Second, security and compliance are no longer differentiators; they are requirements. As transaction volumes rise, platforms are expected to embed controls for AML, KYC, and PCI DSS directly into the payment process. For B2B finance teams, this reduces the need for manual checks and helps standardize how exceptions are handled. (HighRadius, 2026: https://www.highradius.com/resources/Blog/best-cross-border-payment-platforms/)

Third, automation and AI are becoming central to collections efficiency—especially in reconciliation and exception management. The practical pain point in B2B is rarely “taking the payment.” It’s matching it to the right invoice, handling partial payments, resolving discrepancies, and posting accurately to the general ledger. AI-driven workflows are being positioned as a way to reduce manual work, minimize errors, and scale without expanding headcount at the same rate as transaction volume. (HighRadius, 2026)

Evaluate Chile B2B Payments Options

If you’re evaluating B2B payment/collection tools in Chile, map each option to the job you need it to do:

1) Accept & collect (front-end rails): Which customer payment methods must you support (cards, bank transfer, wallet/QR, cross-border)?

2) Control & prove (risk/compliance): What’s built-in vs manual for KYC/AML checks, audit trails, and role-based approvals?

3) Close the books (back-office automation): How well does it handle invoice matching, partial payments, chargebacks/disputes, and ERP/GL posting?

4) Stay resilient (operations): Do you need multi-acquiring, failover options, and clear support/incident processes as volumes grow?

Taken together, these trends push the market toward platforms that behave less like payment buttons and more like financial operations infrastructure—where payments, invoicing, reconciliation, and compliance are treated as one continuous system.

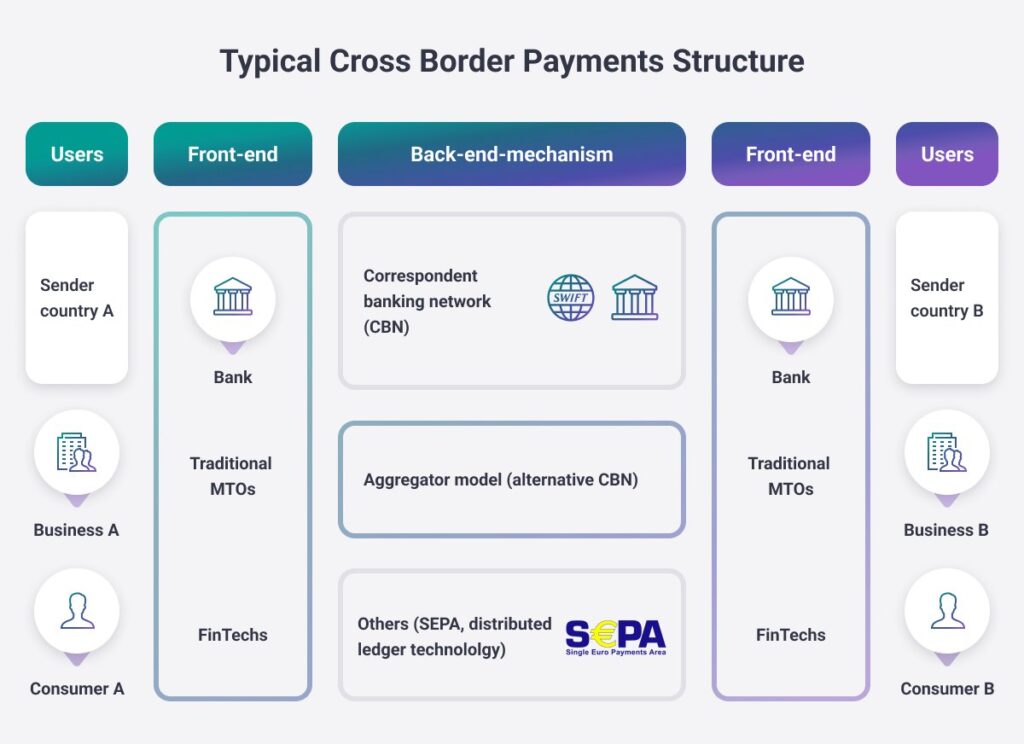

Cross-Border Payment Platforms for Chilean Businesses

As Chilean companies expand internationally, cross-border collections and payments become a distinct operational category—one that demands multi-currency support, FX optimization, and compliance that can withstand scrutiny.

A key reference point in 2026 is the global scale of the opportunity: the cross-border B2B payments market is valued at $1.67 trillion in 2026, growing at a 10.79% CAGR. (HighRadius, 2026: https://www.highradius.com/resources/Blog/best-cross-border-payment-platforms/) Note: market sizing figures are typically estimates based on the publisher’s methodology and may vary across sources.

HighRadius is highlighted as a leading cross-border B2B platform, with capabilities that map directly to enterprise pain points: automated multi-currency reconciliation, dynamic selection of cost-effective payment rails, and real-time invoice matching and GL posting. It also emphasizes AI-powered exception management, targeting the long tail of mismatches and disputes that consume finance teams’ time. (HighRadius, 2026)

A simplified comparison of cross-border options referenced in 2026 coverage looks like this:

| Platform | Key Features | Compliance | Automation | FX Optimization | ERP Integration |

|---|---|---|---|---|---|

| HighRadius | Multi-currency, AI, real-time reconciliation | Yes | Full | Yes | Yes |

| PayU | Global reach, local methods | Yes | Partial | Yes | Yes |

| PayPal | Global, instant, trusted | Yes | Partial | Yes | Yes |

Italic caption: Cross-border B2B platforms commonly considered for international collections and payments (2026).

Cross-Border Payment Approach Tradeoffs

Choosing a cross-border approach usually comes down to what you’re optimizing:

– Wallet-style/global checkout (e.g., PayPal): Faster to deploy and familiar to international payers, but you may trade off on fee control, deeper reconciliation automation, and complex approval/audit workflows.

– Enterprise automation platforms (e.g., HighRadius): Stronger for multi-entity reconciliation, invoice matching, and ERP posting at scale, but typically require more implementation effort and tighter process alignment across finance/IT.

– Hybrid reality: Many teams start with a wallet for “long-tail” international payers, then add automation once cross-border volume (and exception workload) becomes material.

For Chilean businesses, the decision often hinges on whether cross-border is an occasional need (where a global wallet may suffice) or a core workflow (where reconciliation, posting, and controls justify a more specialized platform).

Local Startups Innovating in B2B Payments

Chile’s B2B fintech story in 2026 is not only about large gateways. Local startups are building targeted solutions for recurring collections, merchant acceptance, and credit/payment management—often focusing on the operational details that traditional providers treat as edge cases.

Toku stands out for recurring payments and collections automation. It provides businesses with tools to automate collections and improve customer engagement, including customizable portals and robust automation features. The company’s traction is reflected in funding: it raised $64.6M in Series A and is recognized among Chile’s notable payments startups. (Tracxn, 2026: https://tracxn.com/d/explore/payments-startups-in-chile/__RixS8k1cUIFaLGN9TxRu7zqlDwvVLcwl8U_1yke1qtM/companies)

Pago46 targets merchant acceptance through a mobile-first gateway model, enabling QR code payments, receipts, and merchant commissions, with support for Android and iOS. In a B2B context, QR and mobile acceptance can be relevant for field sales, on-site service providers, or hybrid businesses that collect both in-person and remotely.

Destacame operates in the intersection of credit assessment and payment management, offering tools that facilitate bill payments and business reports. For B2B, this points to a broader trend: payments are increasingly bundled with risk and decisioning, especially where trade credit, installment arrangements, or customer scoring influence collection strategy.

Evaluate B2B Payments Providers

A practical way to evaluate a B2B payments/collections startup (before you commit):

1) Map the workflow: What exactly will it replace—payment acceptance, recurring billing, dunning, reconciliation, or reporting?

2) Integration checkpoint: Confirm how it connects to your invoicing/ERP/GL (and what’s manual if the integration fails).

3) Controls checkpoint: Define who can refund, change bank accounts, edit invoices, or override matches—and how those actions are logged.

4) Exception drill: Ask for a walkthrough of partial payments, chargebacks/disputes, and mismatched references (the “messy middle” of B2B).

5) Exit plan: Clarify how you export data (customers, mandates, invoices, payment history) if you switch providers later.

What these startups share is focus. Rather than trying to be everything to everyone, they aim at specific friction points—recurring collections, mobile acceptance, or credit/payment visibility—then integrate into the broader stack that Chilean businesses already use.

Investment Landscape for B2B Fintech in Chile

Chile’s B2B fintech momentum is supported by an active investment ecosystem that includes both private venture funds and public innovation support. As of January 2026, a set of top B2B-focused investors includes Devlabs, Compusoluciones Venture, CARABELA, ChileGlobal Ventures, and CORFO, among others—backing B2B software, SaaS, and fintech startups. (Shizune, 2026: https://shizune.co/investors/b2b-vc-funds-chile)

A sample of the investor landscape referenced in 2026 includes:

| Investor | Notable Focus | Recent Investments |

|---|---|---|

| Devlabs | B2B, SaaS | 4 B2B deals |

| Compusoluciones Venture | Software, SaaS | 3 B2B deals |

| ChileGlobal Ventures | AgTech, AI, Software | INDIMIN, Altum Lab |

| CORFO | Public fund, innovation | Wareclouds, Altum Lab |

| Fen Ventures | FinTech, Software | Splight Tech, Fecundis |

Italic caption: Selected B2B-oriented investors active in Chile (2026).

For founders, this mix of capital sources can reduce the “valley of death” between early traction and scalable go-to-market. For buyers—mid-sized companies and enterprises—it can be a positive signal that vendors have runway to invest in compliance, integrations, and product depth.

At the same time, the market’s maturation means expectations rise: investors and customers alike increasingly reward platforms that can demonstrate operational resilience, embedded compliance, and measurable efficiency gains in finance workflows.

Future Trends in B2B Payments and Collections

Looking beyond 2026, the direction of travel is clear even if individual winners are not: B2B payments are converging with financial operations.

Open Finance and multi-acquiring are likely to keep pushing the market toward interoperability and redundancy. For businesses, that means less dependence on a single provider and more ability to optimize payment routing, acceptance, and cost—especially as providers compete on reliability and integration depth.

Automation and AI will continue moving upstream. Today, much of the value is in reconciliation and exception handling; next, the competitive edge may be in end-to-end orchestration: invoice issuance, payment reminders, customer self-service portals, real-time matching, and automated posting to the GL—reducing days sales outstanding by removing friction rather than applying pressure.

Compliance-by-design will also deepen. As platforms embed AML, sanctions screening, and PCI DSS controls into workflows, compliance becomes less of a periodic audit scramble and more of a continuous operating mode. For cross-border businesses, this is essential: the cost of weak controls is not only regulatory risk, but operational drag—manual reviews, delayed settlements, and inconsistent customer experiences.

Finally, the market will likely keep segmenting. Some providers will win on breadth (many methods, many countries), while others win on depth (best-in-class reconciliation, ERP integration, or recurring collections). Chile’s advantage is that its ecosystem already supports both models.

Future-Proof Your Payments Stack

What to watch over the next 12–24 months (so your stack doesn’t get outdated):

– Interoperability reality check: Are Open Finance connections actually reducing manual exports/imports for your team?

– Multi-acquiring adoption: Can you add a second acquirer/rail without reworking your entire checkout and reconciliation process?

– Exception automation: Are mismatches, partial payments, and disputes decreasing—or just moving to a different queue?

– ERP/GL depth: Are postings truly automated (with audit trails), or are you still doing spreadsheet-based “bridges” at month-end?

– Embedded controls: Are KYC/AML checks and approval workflows consistent across domestic and cross-border collections?

Final Thoughts on B2B Solutions in Chile

Chile’s B2B payments landscape in 2026 is defined by maturity: more providers at scale, clearer regulatory direction, and a stronger emphasis on operational outcomes—reconciliation speed, compliance confidence, and integration with finance systems.

The practical takeaway for businesses is that “payments” should be evaluated as a workflow, not a feature. The best solution is the one that reduces manual effort, supports the rails your customers actually use, and can scale with your transaction volume and compliance obligations—locally and cross-border.

Practical B2B Payments Implementation Lens

An implementation lens that tends to hold up in real B2B rollouts:

– Start with the “close” problem: If you can’t match payments to invoices cleanly, faster acceptance just creates faster chaos.

– Optimize for exceptions, not the happy path: Partial payments, wrong references, and disputes are where time (and trust) gets lost.

– Treat controls as product features: Approval flows, audit logs, and role permissions are part of the user experience for finance teams.

– Plan for a blended stack: It’s common to combine a domestic-optimized rail with a cross-border tool—then unify reporting and reconciliation.

This perspective reflects a builder’s lens shaped by Martin Weidemann’s work across payments, fintech/insurtech, and multi-industry digital transformation in Latin America, where reconciliation, pricing, fraud/chargebacks, and compliance controls tend to be the real make-or-break details in B2B payment operations.

This article reflects publicly available information at the time of writing and highlights commonly referenced providers and market signals for 2026. Fees, product capabilities, regulatory details, and availability may change, and suitability can vary by business type and integration needs. Before making decisions, confirm current pricing, supported rails, and integration requirements directly with each provider.

I am Martín Weidemann, a digital transformation consultant and founder of Weidemann.tech. I help businesses adapt to the digital age by optimizing processes and implementing innovative technologies. My goal is to transform businesses to be more efficient and competitive in today’s market.

LinkedIn